{kind=link}

Introduction to Blockchain technology

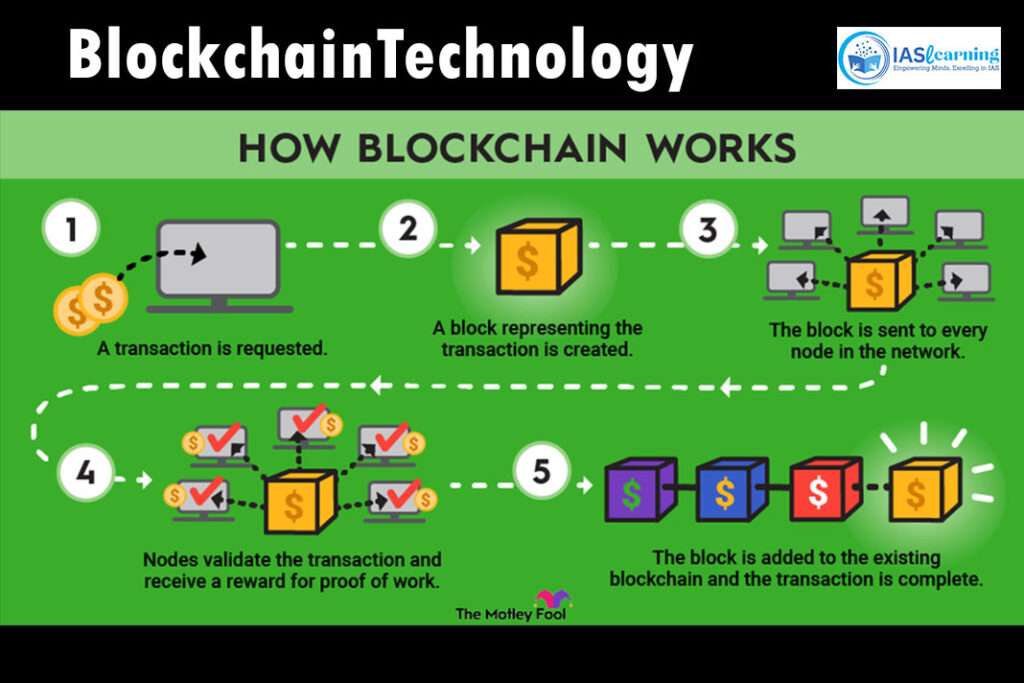

Blockchain technology is a decentralized and distributed ledger system designed to record transactions across multiple computers or nodes.

It is most commonly associated with cryptocurrencies like Bitcoin, where it serves as the foundation for the digital currency’s transaction ledger.

However, blockchain technology has evolved beyond cryptocurrency and has found applications in various industries.

Here are the key components and features of blockchain technology:

Decentralization: Blockchain technology operates on a decentralized network of computers or nodes. Unlike traditional centralized systems where a single entity controls data, blockchain data is distributed across a network. This decentralization ensures that no single party has complete control over the ledger, making it resistant to tampering and censorship.

Immutable Ledger: Once data is recorded on the blockchain technology , it becomes extremely difficult to alter or delete. Each new set of transactions is linked to the previous one through cryptographic hashes, creating an unbroken chain of blocks. This immutability enhances the security and trustworthiness of the data.

Transparency: All transactions on the blockchain technology are transparent and visible to all participants in the network. This transparency fosters trust among users and reduces the risk of fraud or manipulation.

Consensus Mechanisms: Blockchain networks use consensus mechanisms to validate and add transactions to the ledger. These mechanisms ensure that all nodes in the network agree on the state of the ledger. Common consensus mechanisms include Proof of Work (PoW) and Proof of Stake (PoS).

Cryptographic Security: Blockchain employs cryptographic techniques to secure data. Each participant on the network has a pair of cryptographic keys: a public key and a private key. The private key is used to sign transactions, while the public key is used to verify them.

Smart Contracts: Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automate contract execution and enforce agreements without the need for intermediaries, such as lawyers or banks.

Peer-to-Peer Transactions: Blockchain technology enables peer-to-peer (P2P) transactions without the need for intermediaries like banks or payment processors. This reduces transaction costs and speeds up settlement times.

Use Cases Beyond Cryptocurrency: While blockchain technology originated with Bitcoin, its applications extend far beyond cryptocurrency. It is used in supply chain management, healthcare, voting systems, identity verification, real estate, and more.

Tokens and Digital Assets: Many blockchain networks facilitate the creation and exchange of tokens and digital assets. These tokens can represent ownership in assets, access to services, or even voting rights within a network.

Permissioned and Permissionless Blockchains: Blockchains can be either permissioned (private) or permissionless (public). Permissioned blockchains restrict access to authorized participants, while permissionless blockchains are open to anyone.

Advantages of Blockchain technology

Security: Blockchain is highly secure due to its cryptographic features. Once data is added to the blockchain, it becomes extremely difficult to alter or delete. Each block contains a cryptographic hash of the previous block, creating a chain of blocks that is resistant to tampering and fraud.

Transparency: All transactions recorded on the blockchain are visible to all participants in the network. This transparency fosters trust among users and allows for real-time auditing of transactions.

Decentralization: Blockchain operates on a decentralized network of computers or nodes. This means there is no central authority or single point of control. Decentralization enhances the security and resilience of the network, as there is no single point of failure.

Immutability: Once data is recorded on the blockchain, it cannot be easily changed or deleted. This immutability ensures the integrity of the data, making it ideal for applications where data integrity is critical.

Reduced Intermediaries: Blockchain enables peer-to-peer transactions without the need for intermediaries like banks or payment processors. This reduces transaction costs, speeds up settlement times, and eliminates the need for third-party trust.

Efficiency: Blockchain can streamline processes by automating tasks through smart contracts. These self-executing contracts automatically enforce the terms of agreements, reducing the need for manual intervention and paperwork.

Traceability and Auditing: In supply chain management and other industries, blockchain provides a transparent and immutable record of the origin and movement of goods. This traceability simplifies auditing and helps in quickly identifying the source of any issues or defects.

Global Accessibility: Blockchain networks are accessible from anywhere in the world with an internet connection. This makes blockchain-based services and applications globally available, expanding access to financial services, information, and more.

Data Privacy: Blockchain allows users to have greater control over their data. Users can grant or revoke access to their data as needed, enhancing privacy and data security.

Tokenization: Many blockchain networks support the creation and exchange of tokens. These tokens can represent ownership in assets, access to services, or voting rights within a network, providing new opportunities for value creation and ownership.

Resilience: Blockchain networks are designed to be highly resilient and fault-tolerant. They continue to operate even in the face of network disruptions or attacks.

Innovation: Blockchain technology has spurred innovation across industries. It has paved the way for new business models, applications, and decentralized ecosystems.

Financial Inclusion: Blockchain can provide access to financial services for individuals who are unbanked or underbanked, allowing them to participate in the global economy.

Trust: Blockchain’s transparent and tamper-proof nature fosters trust among users. It reduces the need for trust in intermediaries, making transactions and agreements more secure and reliable.

Reduced Fraud: Blockchain’s security features make it difficult for bad actors to manipulate data or engage in fraudulent activities.

Applications of Blockchain

Cryptocurrencies: Cryptocurrencies like Bitcoin and Ethereum use blockchain as their underlying technology to enable secure, peer-to-peer digital transactions without the need for traditional banks or financial intermediaries.

Smart Contracts: Smart contracts are self-executing contracts with predefined rules and conditions directly written into code. They automate contract execution and eliminate the need for intermediaries in legal and business agreements.

Supply Chain Management: Blockchain is used to track the movement and origin of goods in supply chains. It provides real-time visibility into the production, shipment, and delivery of products, enhancing transparency and reducing fraud.

Digital Identity: Blockchain-based identity systems offer secure and verifiable digital identities. Individuals have more control over their personal information and can share it with trusted entities as needed, reducing identity theft and fraud.

Voting Systems: Blockchain can be used for secure and transparent electronic voting systems. It enhances the integrity of elections by reducing the risk of tampering and ensuring that votes are accurately recorded.

Healthcare: Blockchain secures and manages electronic health records (EHRs) by providing a tamper-proof ledger. Patients can grant access to healthcare providers while maintaining control over their data.

Real Estate: Blockchain simplifies property transactions by securely recording ownership and transaction history. It reduces fraud and speeds up the transfer of property titles.

Cross-Border Payments: Traditional cross-border payments can be slow and costly. Blockchain technology enables faster and more cost-effective international money transfers.

Tokenization of Assets: Assets such as real estate, art, and stocks can be tokenized on blockchain platforms, allowing for easier trading, increased liquidity, and fractional ownership.

Intellectual Property: Artists and creators can use blockchain to secure intellectual property rights and ensure fair compensation for their work through transparent and automated royalty distribution.

Energy Trading: Blockchain enables peer-to-peer energy trading by recording and verifying energy transactions on a distributed ledger. It allows individuals to buy and sell excess energy directly to one another.

Agriculture: In the agricultural sector, blockchain can track the origin and journey of agricultural products, helping to identify and address issues like contamination or spoilage.

Education: Blockchain can verify and share academic credentials and certifications, making it easier for employers and educational institutions to verify the authenticity of qualifications.

Charity and Aid: Blockchain enhances transparency in charitable donations and aid distribution. Donors can track how their contributions are used, and aid can be distributed more efficiently.

Legal and Notary Services: Legal documents and notarization services can be recorded on the blockchain, providing an immutable record of agreements and reducing the need for traditional notaries.

Media and Content Distribution: Blockchain offers decentralized content distribution platforms, enabling creators to share content without the need for intermediaries, and ensuring fair compensation through microtransactions.

Applications of Blockchain Technology

| Some examples of Global Adoption of Blockchain | |

| Estonia | It is the world’s blockchain capital and is using blockchain infrastructure to verify and process all e-governance services offered to the general public. |

| China | It launched BSN (Blockchain-based Service Network) to deploy blockchain applications in the cloud at a streamlined rate. |

| Britain | There is a National Digital Twin program to foster collaboration between owners and developers of digital twins in the built environment. |

| Brazil | Brazilian government launched Brazilian Blockchain Network to bring participating institutions in governance and the technological system that facilitates blockchain adoption in solutions for the public good. |

National Strategy on Blockchain

- National Strategy on Blockchain has been formulated by Ministry of Electronics & Information Technology (MeitY) with the vision to create trusted digital platforms through shared Blockchain infrastructure; promoting research and development, innovation, technology and application development; facilitating state-of-the-art, transparent, secure and trusted digital service delivery to citizens and businesses.

- This strategy lays out overall vision towards development and implementation strategies for a National Blockchain Platform covering the technology stack, legal and regulatory framework, standards development, collaboration, human resource development and potential use cases.

Challenges Associated with Blockchain Technology

Scalability: One of the most significant challenges is scalability. Public blockchain networks like Bitcoin and Ethereum can become slow and costly to use as more users join the network. This is because every transaction needs to be validated by every node on the network. Solutions like sharding and layer 2 scaling are being explored to address this issue.

Energy Consumption: Proof of Work (PoW) consensus algorithms, used by Bitcoin and Ethereum, require significant computational power and energy consumption for mining. This raises environmental concerns and can be expensive. Transitioning to more energy-efficient consensus mechanisms like Proof of Stake (PoS) is a potential solution.

Interoperability: Different blockchain networks often operate in isolation, making it challenging to exchange data and assets between them. Interoperability standards and protocols are being developed to bridge this gap.

Regulatory Challenges: Blockchain’s decentralized and pseudonymous nature poses challenges for regulators. Governments are working on establishing regulatory frameworks to address issues like taxation, fraud, and illicit activities conducted using cryptocurrencies.

Privacy Concerns: While blockchain provides transparency, it can also expose sensitive information. Privacy-focused blockchains and zero-knowledge proofs are being developed to address privacy concerns.

Lack of Legal Clarity: Legal issues related to smart contracts and digital assets are still evolving. The enforceability of smart contracts and the classification of tokens vary from one jurisdiction to another.

User Experience: Blockchain applications often have a steep learning curve and can be challenging for non-technical users. Improving the user experience is crucial for mainstream adoption.

Security Risks: While blockchain is considered secure, vulnerabilities in smart contracts, software bugs, and human errors can lead to security breaches. Regular audits, code reviews, and security best practices are essential to mitigate these risks.

Cost: Implementing and maintaining blockchain networks can be costly, particularly for small businesses and startups. Cost-effective solutions and cloud-based services are emerging to address this challenge.

Lack of Standardization: The absence of global standards in blockchain technology makes it challenging to develop interoperable solutions and hinders collaboration between different projects.

Adoption Barriers: Convincing established industries to adopt blockchain technology can be difficult due to resistance to change and the need for significant infrastructure updates.

Environmental Concerns: As mentioned earlier, PoW blockchains like Bitcoin have high energy consumption. This has raised concerns about the environmental impact of blockchain technology.

Legal Identity: Blockchain-based identity systems, while promising, face challenges related to verifying real-world identity and ensuring protection against identity theft.

Data Storage: Storing data on a blockchain can be expensive, especially for large volumes of data. Solutions like decentralized storage networks are emerging to address this challenge.

Oracles and Real-World Data: Smart contracts often rely on external data sources, called oracles, for real-world information. Ensuring the accuracy and security of these oracles is a challenge.

Way Forward

Transition to Sustainable Consensus Mechanisms: Shift from energy-intensive PoW to more environmentally friendly consensus mechanisms like PoS and delegated PoS. These mechanisms can reduce the carbon footprint of blockchain networks.

Regulatory Frameworks: Collaborate with governments and regulatory bodies to establish clear and balanced regulatory frameworks that encourage innovation while addressing concerns related to fraud, taxation, and illicit activities.

Privacy Enhancements: Invest in privacy-focused blockchain solutions, zero-knowledge proofs, and privacy-preserving smart contracts to ensure data confidentiality while maintaining transparency.

Improved User Experience: Focus on improving the user experience of blockchain applications to make them more accessible to non-technical users. This includes user-friendly wallets, interfaces, and educational resources.

Security Best Practices: Implement rigorous security practices, including regular code audits, formal verification, and education on secure development practices to reduce vulnerabilities and security breaches.

- Blockchain Adoption in Education: The adoption of blockchain in education could improve the efficiency of the education ecosystem and optimise the use of human and physical resources. It can also address concerns such as data privacy, cost, scalability and integration with legacy systems.

- Investment for Digital Education: Transition to digital education needs multi-pronged efforts, investment and better infrastructure for students, teachers and institutions. Stakeholders such as educational institutions, prospective employers, mentors and certification agencies can create a robust digital education ecosystem with blockchain.

- Robust Policy for Blockchain Development: Government policy for blockchain development should focus on facilitating technological expertise, attracting better investments and encouraging all stakeholders for social and economic growth through the help of blockchain development.